“Trumpflation” Risks Likely Overstated by Lance Roberts via Zerohedge:

The question is whether policies being considered by the next Presidential administration will lead to “Trumpflation” or not.

…

Current Thinking

Many mainstream economists and analysts believe President Trump’s economic policies could trigger “Trumpflation.” The term refers to potential inflation driven by his administration’s fiscal and trade policies. Analysts suggest that extending the TCJA tax cuts, further tax cuts, infrastructure spending, or increased military budgets will boost economic growth and lift inflation. The belief is that this fiscal stimulus, especially during an already low unemployment environment, would increase demand, leading to price increases.Furthermore, “Trumpflation” could be triggered by introducing trade protectionism and tariffs. Economists argue that restricting imports and raising tariffs on foreign goods will lead to higher domestic prices, as the costs of imported goods would rise. Combined, these policies pointed to risks of higher consumer prices and potentially higher interest rates.

The advantage that we have today is that we can review President Trump’s first term to see if the same policies instituted then led to higher interest rates and inflation.

The problem with reasoning this way is that Mr. Roberts is looking at what actually happened, not what happened relative to the counterfactual, or what economists parsed out as what happened as a result of the measures undertaken by Mr. Trump during his first administration using econometric methods.

What is true is that predictions of higher inflation are conditional on passage of the proposed measures (as modeled by the modelers), and the models themselves. So deviations from predictions can happen because the assumptions of what happens (invasion, war, measures fail in congress) vs. the models.

What about reasoning from what happened in 2018. The proposals are different. A 10% overall tax on imports and 60% tariff on Chinese imports is different from selective tariffs on steel and aluminum (Section 232), and tariffs on Chinese goods under Section 301.

Mr. Roberts also goes into a long discursion into why tax cuts (and/or maintaining TCJA cuts) isn’t going to be inflationary, noting that increased debt-to-GDP hasn’t been correlated with higher yields. Well, that’s reasoning by correlation. What needs to be assessed is whether rising debt issuance will be matched by rising demand for Treasurys either domestically or by foreign holders. In the past, the US has been bailed out by the foreign sector avidly buying up Treasurys. Can we rely upon that in the future? Maybe, maybe not. If interest rates go up, then (given Mr. Trump’s desire to have bigger say in interest rates), the Fed might be forced to keep monetary policy more accommodative to (expansionary) fiscal policy, and that means (over time) higher inflation than would have otherwise occurred.

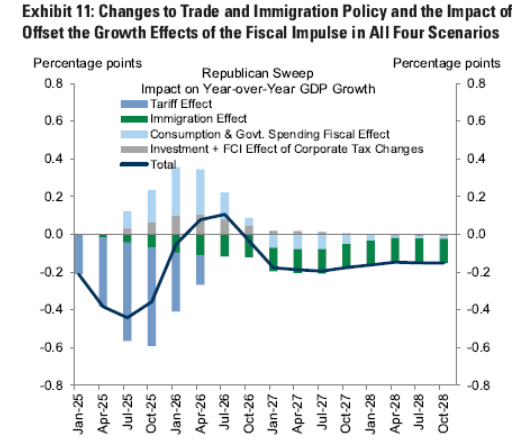

So, for my part, I’m more partial to this set of scenarios (from Goldman Sachs, discussed here):

Note that these are differences relative to baseline.

On March 3, Mobile World Congress will kick off in Barcelona, Spain. While it’s not…

Sentiment gauges have soured — but the S&P 500 was at record highs just a…

Kalshi betting right now is for 300K reduction in force for the Federal government (h/t…

The witness discount refers to the reduction in data “weight” given to the witness portion…

In spite of the Tesla CEO's best efforts, the AfD performed no better than had…

© 2025 Fortune Media IP Limited. All Rights Reserved. Use of this site constitutes acceptance…

{kind=link}